Bubble trouble will trigger a more aggressive BoJ

When will asset inflation in general, home affordability in particular, become a political force demanding accelerated rate hikes?

By popular request, here my thoughts on what dynamics will force the Bank of Japan to actually accelerate rate hikes — it’s not the falling Yen; it’s not ‘fiscal dominance’ and fear of rising public debt-services costs versus asserting central bank independence; but watch out for when Japan’s elite begins to openly complain about home affordability. Not now, but the time will come…I maintain my expectations for BoJ policy rates to rise towards 2.5% to 3% by the time Governor Ueda’s term ends in April 2028.

Remember BoJ Governor Mieno…

The most impressive and consequential policy speech I ever witnessed was given by the then newly appointed BoJ Governor Mieno on December 19, 1989:

“Thank you for entrusting in me to the important position of central bank governor. Bad things are happening in our country: A new graduate of the best university entering the best Japanese company can no longer dream of ever being able to afford buying a home within a two-hour commute to his company. This is bad, this is a bubble, and I will burst it”. (or words to that effect, from my diary).

And burst the bubble he did. In less than nine months, he raised the official discount rate from 3.75% to 6%. 10-year JGBs peaked at 8.3% at the end of September 1990 - a full nine months after the Nikkei had peaked at just below 40,000. And yes, within ten years after Governor Mieno’s promise to bring back the dream of homeownership to the next generation, Japan had destroyed more balance sheet wealth than she had lost during the Pacific War.

Governor Mieno is often remembered for doing “too little, too late” to counter asset deflation; yet his primary legacy is that he actually did what only the very best central bakers do: “take the punchbowl away when the party got out of hands”. Importantly, his hero, Fed chair Paul Volker, had done so to crush consumer price inflation - a perfectly orthodox reason for a central banker. In contrast, Governor Mieno himself did so explicitly to crush asset inflation - a very unorthodox reason - if not outright anathema - to most anglo-American experts. And yes, Japan’s ruling elite stood firmly behind him when he did so.

Clear speak: Asset price inflation worship has clear limits in a culture where the elites’ obligations to the nation are grounded in a loathing of avarice, selfishness and plutocracy. Don’t get me wrong: it is not that Japanese elites are not ‘greedy’; but being humble and exemplary carries an even higher premium…..if (when?) Japan wins the World Cup, the then obviously best and most aggressive team in the world will still clean up their locker rooms by themselves, serving as inspiration for their fans to clean up the stadium…to inspire the world, Pax Nipponica.

Be this as it may.

Let’s focus on the affordability metrics - is the current rise in asset prices in general, the real estate market in particular pricing out the next generation’s dream of home-ownership? How close are we to ‘bubble trouble’ triggering the elites obsession with social harmony?

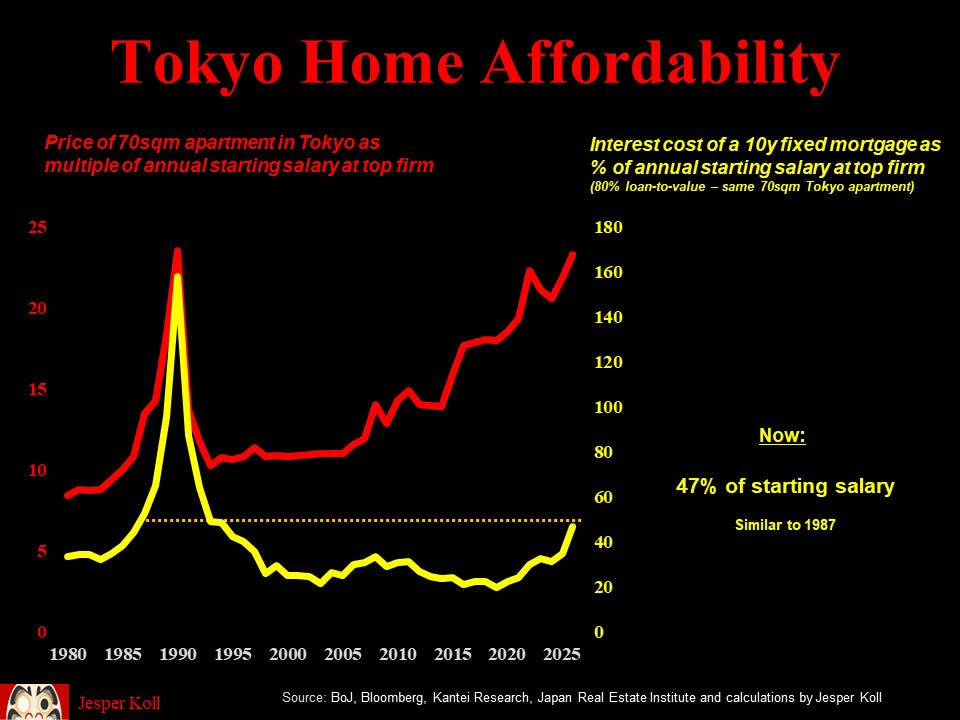

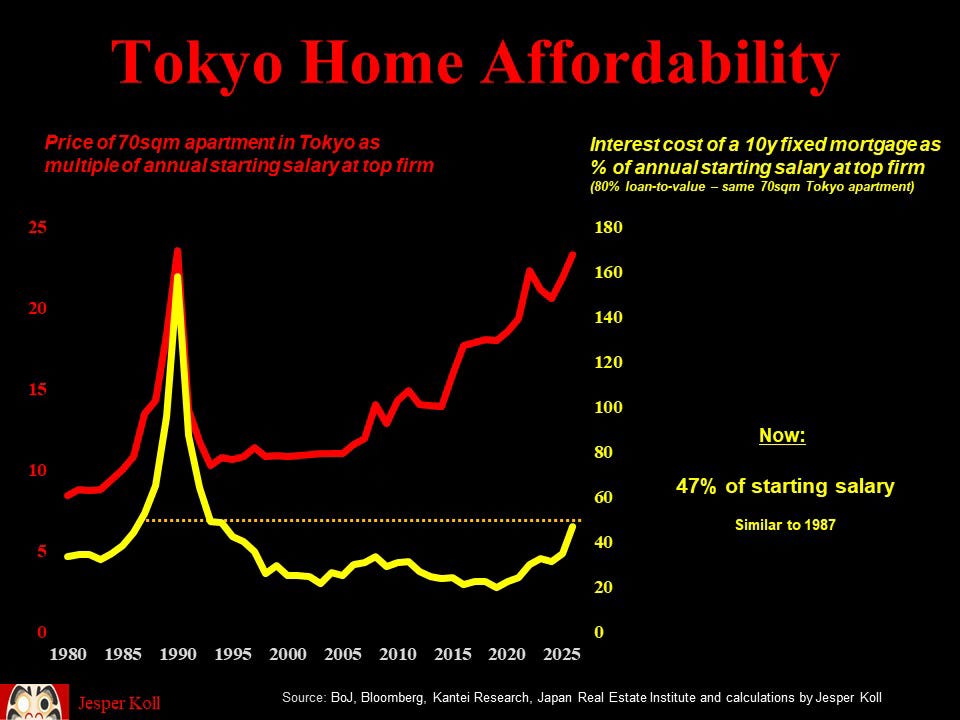

Taking a clue from the Mieno speech: a new graduate hire at Japan’s top firm now can buy a typical 70 square meter apartment in Tokyo with 23-years worth of his/her annual income - basically exactly what it took at the bubble peak in 1990. Before the 1980s bubble, it took 5-7 years….23-years now, just as bad as it was when Governor Mieno started his attack on the bubble.

Of course, in the real world affordability is also determined by mortgage costs. Here the affordability metrics are slightly better, but not by very much:

Taking the same typical 70-square meter Tokyo apartment and financing it with a 15-year mortgage and the typical 80% loan to value, now costs you 47% of your starting income. Yes, well below the 160% (!) required at the 1990 bubble peak; but still up from barely 20% five years ago. In fact, today’s 47% of income going to service your mortgage is exactly where we were in 1987…which then was also up almost double from where it had been five years before. Here the chart again:

Many forecasters try and argue that this deterioration of mortgage financing cost forced by rising property prices is one reason for the BoJ to go slow. This is a potentially dangerous misunderstanding of the elites’ priorities. They will, in my view, not hesitate to “take the punch bowl away” when social harmony comes under stress with the next generation complaining about not being able to buy their dream.

BUT: 2026 national priorities are very different from what they were in 1989

To be sure, Governor Ueda is no Mieno. More importantly, Japanese elites’ anger at the bubble’s bad influence on social harmony was very broad based and deep in the late-1980s. This is not the case now, so the pressure for the BoJ to act more aggressively is not there.

Specifically, a year before Mieno’s appointment, the Recruit Scandal broke in June 1988 — the start-up wunderkind and ‘move fast and break things’ face of the then ‘new Japan’ Ezoe Hiromasa, founder of Human Resources conglomerate Recruit, had offered deeply discounted pre-IPO shares of his real estate subsidiary Recruit Cosmos to 76 elite politicians. By May 1989 Finance Minister Miyazawa and Prime Minister Takeshita and his cabinet resigned in disgrace.

Today, the elites priorities are first and foremost focused on mobilizing domestic resources to ensure greater national security, sovereignty and resilience against geoeconomic shocks and potentially unreliable allies. This is best achieved under inflation — free capital for the levered, for the risk-takers & builders, and good for the treaury because inflation boosts tax revenues. Make no mistake: Inflation is now in Japan’s national interest. Let China deflate while Japan inflates.

Importantly, the elites are convinced that both public sector regulatory & oversight reforms and private sector governance reforms have significantly reduced the risks of greed and bubble excesses. No Recruit Scandal likely.

Still: watch out for a change in rhetoric. Japan will never, in my view, raise interest rates to defend the Yen from depreciating; but they will raise rates when Prime Minister Takaichi pivots to ensure the young generation can realize its dream of homeownership. The time is not now, but it will come before long.

Meanwhile, BoJ Governor Ueda will continue to gradually raise rates - his goal now is to find the “neutral” policy rate before he leaves office. Modest inflation, yes; a bubble that his successor will be forced to burst, no. A clean locker room and a clean stadium…

thank you for reading. As always, comments welcome. Many cheers from is-it-rainy-season-yet? Tokyo ;-j

Do remember the late 80's bubble and it's peak. Is such bubble limited to Tokyo or a nationwide problem? Is this just for such type of housing (under 100 sqm). Does the real estate ownership structure concentrated?