Japan reality check #1: how does Japan Inc. distribute its spoils?

Shareholders get the lions share, while investment in productive assets has stagnated

New series from Japan Optimist - every ten days or so, a chart to help focus and stimulate the Japan narrative.

Global investors have been relentless in their calls for better corporate governance in general, higher payouts for shareholders in particular. However, a reality check reveals that Japan Inc’s primary problem is not a disregard for shareholders, but a stubborn refusal to invest in both physical- and human productive capacity.

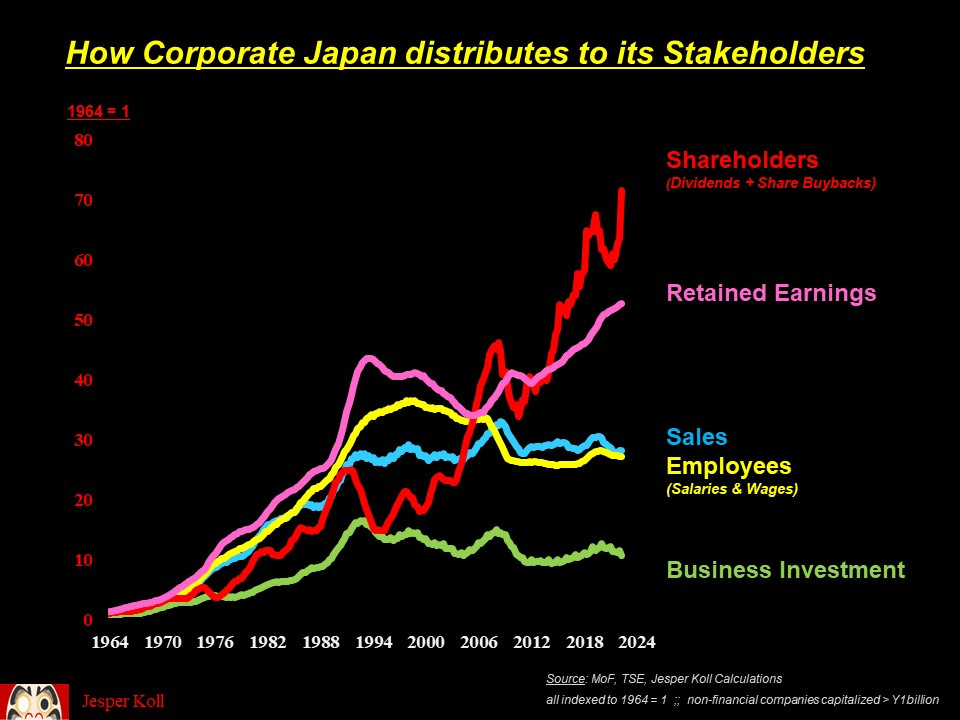

Really? Here is how Japan Inc. has distributed to the key stakeholders since 1964.

(The underlying data set covers Japan’s large, primarily listed non-financial companies; the chart shows the cumulative growth for each variable; all as multiples of the 1964 starting point. Specifically, in 2022 sales were 27-times higher than they were in 1964, and returns to shareholders - dividends & share buybacks - stood 72-times above 1964 levels, well ahead of returns to labor, up 36-times, or investment into the business, up barely 11-times.)

So the evidence is clear: the leaders of Japan Inc. are actually very shareholder focused; but, since the early 1990s, they have lacked the basic ambitions - the greed? the vision? the optimism? - required of good capitalists: CEOs and their boards prefer to hoard cash rather than invest in the factors of production that could grow the business and raise prosperity for all stakeholders.

Some highlights, comparisons, and thoughts:

From top-line…

Any corporate analysis starts with sales, the top-line for any enterprise. And top-line reality has been harsh - sales of Japan’s large and publicly listed non-financial firms have basically flatlined for three decades: in 2022 total sales were just about where they were in 1994. In contrast, sales of large U.S. companies (those in the S&P500 index) rose 2.5-times between 1994 and 2022. How many U.S. companies would survive three decades for zero growth in sales?

…to winners

With or without sales growth, the distribution data reveals which stakeholder of Japan Inc. gets a bigger or smaller part of the spoils — shareholders (red line); the company’s ‘war chest’, i.e. retained earnings (pink line); or the company’s current and future growth potential potential, i.e. employees (yellow line) or investment (green line). Importantly, the distributions here do get decided by corporate leaders

The big winner has been returns to shareholders: growth of dividends plus share buybacks has significantly outpaced all other distributions, even retained earnings.

Interestingly, the prioritization of shareholder returns accelerated sharply during 2005-2010, well before the corporate governance- and capital stewardship codes were formalized (the former was first finalized in March 2015; the latter in 2013).

What happened? It was in 2006/2007 that Japan Inc. was challenged by the first wave of high-profile, professionally run activist investor campaigns: the Murakami Fund from within, Steel Partners from overseas.

So shareholder activism actually works in Japan; and more fundamentally, this does suggest Japan Inc. functions exactly the way a free-market capitalist system is supposed to: pioneer investors beat a path that the establishment eventually institutionalizes and follows (1).

Against this, the focus on accumulating retained earnings — basically what’s left after management pays all costs, investments, taxes and dividends — has remained exactly what it has always been: the stand-out top-priority for corporate leaders.

With or without sales growth, with or without new governance- or stewardship codes, Japan’s corporate boards are obsessed with growing retained earnings. Call it prudent or ‘risk-averse’ capital management at its best; or lazy salaryman CEOs and clueless boards without ambitions or vision at its worst - feel free to pick sides. The only thing I know for sure is that here we have the fundamental enigma of Japanese capitalism. A Nobel Prize for applied economics should be awarded to whoever can solve it.

…and losers

In sharp contrast to the structurally entrenched winning streak of retained earnings, there is no uncertainty about who are the losers. The stubborn refusal of corporate leaders to invest in both human- and physical productive capital is, well, shocking:

Investment in labor has not stagnated, but has actually fallen: employee wages & salaries peaked at approximately Y110 trillion in 1998 and dropped to approximately Y85 trillion last year - a level last seen in 1988. Yes: the leaders of Japan Inc. today spend as much on human capital as they did one generation ago.

Investment in productive capital has had some cyclical upturns (forced mostly by replacement cycles), but still the basic trend is one of at least 20-years of stagnation. In contrast, American companies have increased their capex business investment spending by almost 3-times in the past twenty years.

Clear speak : Japan Inc. is significantly underinvested. It is lacking both physical and human productive capacity — not because of some demographic destiny or aging society or lack of children; but because corporate leaders’ steadfast refusal to invest in productive assets in general; labor, technology and capacity to scale in particular.

You don’t have to be an economist to realize that if you consistently don’t invest in the factors of production -employees and capital- your business has no future. Often when debating this dynamics with Japanese establishment leaders, I get pulled towards a “chicken or egg” line of question: is there no sales growth because there is no investment or wage hikes? Or is there no investment or wage hikes because there are no prospects for sales?

Rather than getting into a long argument, I then quote one of the greatest capitalists and business leaders of all times, Henry Ford:

In 1914, Henry Ford announced he’d double the pay of his workers to $5 a day, more than twice the average wage for automakers then; at the same time he also cut the work day from 9 hours to 8 hours. The original plan was to go up to $4.8 per day, but one of his outraged board members complained: ‘why not make it $5 and bust the company right?” “Fine,” said Henry Ford. “We’ll do that”. And no, the company did not go bust but became one of the greatest prosperity creating machines in economic history.

The macro impact of micro action is real. Again, Henry Ford puts it best: “We pay higher wages so that our workers can buy our cars…and if we raise the buying power of our own people, they increase the buying power of other people…it is this thought of enlarging buying power by paying high wages and selling at low prices that is behind the prosperity of this country.”

Clearly, Japan Inc. could do with some of Henry Ford’s simple and practical leadership — nothing new needed, just good old capitalism….

And the good news?

The good news is that past performance is unlikely to be a good guide to the future.

Specifically, in my view, the following key dynamics are now commanding a fundamental about-turn of corporate leadership priorities:

Japanese labor is now not just scarce, but increasingly aware of its value. As the war for talent intensifies, so does the brain drain away from poorly managed companies towards labor empowering, better paying and well-managed ones. The net effect: investment in human capital is poised to rise.

Already, leading companies like NTT are breaking with the proud tradition of seniority-based pay and prepare to introduce merit-based pay- and promotion from this year. Watch for a rise in labor mobility to verify -or falsify- this thesis.

The rise in global prices is now forcing cost-push inflation and profit margin squeezes. Companies not investing in better production technology, new products, better marketing campaigns or new strategic partnerships will get squeezed out of business. Here, the surge in actually applicable new business solutions offered by new technologies adds to the urgency, as does the surge in venture capital and start-ups.

Disruption is coming to Japan. Watch for both, a rise in bankruptcies and a rise in business investment. The former frees up resources and market share that the latter will absorb and put to more productive use.

The new realities of the US-China strategic competition now force new investments in production capacity. Whether on-shoring or friend-shoring, the reallocation of the global productive machine makes imperative a structural up-lift in Japanese business investment. Global ‘business as usual’ is no longer an option for any corporate leader in Japan.

Moreover, the end of the “free ride” and start of greater self-reliance in Japan’s national security and defense policy will turn into a catalyst for new marginal investment spending by both the public- and private sector.

So we’ve got three very powerful new forces: a historically unprecedented ‘war for talent’ in Japan’s most important national asset, her people; a fundamental turn from deflation to inflation that is poised to accelerate creative destruction; and finally, a historic shift in the “guns or butter” resource allocation priorities of the nation.

All said, scarcity is coming to Japan; and scarcity is the exact opposite of what the leaders of Japan Inc. faced during the previous 30-years. Then there was too much labor, too much capacity, too much debt, and too much competition from first Korea and then China. Now there is not enough talent, outdated technology, and an urgency to build a more self-reliant nation. In my view, Japan’s leaders have both the resources and the ambition to rise to the challenge. And the enormous pool of retained earnings alone should guarantee that a newfound investment drive can actually turn into a sustainable win-win for all stakeholders.

What can go wrong?

The principal risk to my ‘good news’ optimistic outlook comes from the government.

The immediate threat is an overzealous treasury insisting on tax hikes. If gains to the purchasing power of the people from rising wages get siphoned off to fund public debt-repayment or interest expense, a Henry Ford style virtuous cycle cannot begin.

A more structural threat is the strong preference of the government to prevent ‘creative destruction’. Already approximately 12% of companies cannot cover their interest expense from current profits, but they are still kept afloat by government support. The optimist scenario depends on a gradual but steadfast withdrawal of government support for “zombie” companies. Productive companies need their market share, their customers, and their resources to build up scale, boost productivity, and earn higher profits.

Re-directing public sector priorities away from the now deeply entrenched and politically expedient support-for-the-weak priorities is poised to be Japan’s biggest structural challenge.

Here, it may well be that we’ll need to see an unintended consequence of the new national security priorities: how long before the ruling LDP will have to - or is prepared to - abandon its “zombie company” constituency to fund Japan’s rising defense spending?

While I doubt LDP priorities and vested interest interests will change soon, I am convinced the priorities of corporate leadership are poised to change faster than generally expected — just as they did in 2005-2010 for shareholder returns.

If I am right and allocations to labor and capital are about to enter a structural up-turn, Japan’s potential growth rate will begin to rise with it. And no, investing for future growth does not come at the expense of lower returns to shareholders…

Thank you for reading. As always, comments welcome. Many cheers ;-j

(1) Initially, the establishment fought back very hard with high costs for the pioneers: Murakami was convicted of insider trading, and Steel Partners lost its case in the High Courts. Now the establishment - the GPIF public pension fund, the big trust banks etc. - are increasingly outspoken champions of more pressure on corporate managers.)

Interesting signal from Fast Retailing about valuation of human capital https://www.bbc.com/news/business-64232184

Just curious, have you played around with the starting date of your time line (1964), and checked whether that would make any difference in the outcome?