Three Cheers for Governor Kuroda

Three Cheers for Governor Kuroda

The Bank of Japan is right to de-couple from America: Japan's monetary policy priorities, domestic demand realities, and what to watch out for from here

June 19, 2022

Here I present some thoughts on the current priorities of Japanese monetary policy. Specifically, I focus on demand. I do so because I take Governor Kuroda at his word – he wants to see demand-pull inflation before he’ll consider a change in policy. He is thus — in my view correctly — focused on what actually drives price increases, rather than the inflation level changes these forces deliver. And he is right in his conclusion: in sharp contrast to America, there is basically no evidence of demand-pull inflation in Japan. And no, supply shocks are never and nowhere a monetary phenomenon (1).

Capitulating to populist or financial market pressure — “just follow the Fed, shut up and fall in line, Kuroda-san” is what many of the worlds leading money managers and economists appear to be calling for — would not just be an insult to the Governor’s deep understanding of history, economic theory, and his second-to-none insights into the art of monetary policy making in the real world. More importantly, it would be a grave error. Capitulation now would deny Japan a once-in-a-generation chance to escape from the deeply entrenched deflation dynamics.

Well, I fully understand if this opening paragraph scares you away from reading the entire piece, so here a quick summary of the analysis and its practical implications :

The inflation rate in both America and Japan has risen by about the same factor over the past 9-12 months: Japan’s is up six fold from around 0.4% to around 2.5%; America’s is up from around 1.4% to now 8.6%, i.e. up a similar 6x.

In sharp contrast, Japan’s nominal GDP is stuck stagnating at approximately 3% below the pre-pandemic trend, while America’s is almost 8% above it, and still accelerating smartly.

This de-coupling of economic cycles is almost entirely due to weak and sub-par consumption in Japan. Importantly, this is in spite of the fact that Japanese disposable incomes are back up to the pre-pandemic uptrends. The Japanese still prefer to save rather than spend.

Mr & Mrs Watanabe did re-open their wallets for a strong recovery in goods spending, and it is the lack of services consumption that accounts for all of Japan’s current domestic demand deflation gap.

Good news - it is actually quite straightforward from here: domestic travel, or rather lack thereof, accounts for the entire gap in domestic spending. So if you want to predict when the BoJ will get ready to change, watch carefully for signs of a pick-up in domestic travel.

Remember the basic facts: domestic travel is almost four-times more important than the much discussed inbound tourism: if domestic travel spending gets back to 2019 pre-pandemic levels, we’d get approximately Y15 trillion of new consumption; a much smaller Y4 trillion is what an inbound tourist recovery back to the 2019 peak could deliver. And unlike global travel, which can be controlled by government policy, domestic travel is de-facto at the full discretion of private citizens, i.e. it is a `true` indicator of consumer confidence and household spending patterns getting back to normal.

When will this be? The mid-August Obon family holidays and the October Momiji autumn travel seasons are key, particularly since typically Japan`s elderly account for most of the spending. One-in-four Japanese is now over 69, and only when this cohort re-opens its wallets, will demand-pull get real.

Bonus: a weak yen will help domestic travel. The more expensive Hawaii, the more attractive Okinawa or Hokkaido become…

I stick with my forecasts for a currency overshoot towards Y150-160/$ as the forces that got us from Y110-115/$ to Y130-135/$ are poised to stay in play: Japan-US interest rate differential will keep widening and Japan`s balance of payments will keep on deteriorating. Both are poised to stay in play at least until the end of this year/early next year.

Well, here we go for the complete main attraction:

Three Cheers for Governor Kuroda

Bank of Japan (BoJ) Governor Kuroda deserves to be congratulated. His steadfast determination to fight Japan’s fight against deeply entrenched deflation on his own terms, without wavering or capitulating to populist or financial market pressures, makes it increasingly likely he’ll enter history as the man who’ll succeed where everyone before him has failed. The longer he insists on de-coupling Japan’s monetary policy from the US’s, the quicker the end of deflation is coming into sight.

Governor Kuroda is right to resist the temptation of following the Federal Reserve of America (Fed). While coordination, conformity and acting in a united front may very well command a new premium in international relations or national security matters, macro economic policy in general, monetary policy in particular must be conducted in a sovereign and independent way.

In fact, the whole rationale behind the free market global financial system is that it allows for national sovereignty. Japan is neither part of the policy straightjackets imposed on the Eurozone members, nor a tributary to the centrally controlled financial system of its largest trade partner, China. Japan is a proud member of the US$ block precisely because it is the only one anchored in freedom and national independence; and yes, the free flow of capital and the foreign exchange market are the structure that guarantee this freedom and enable it.

The makings of a reverse Plaza Accord…

In a way, Governor Kuroda is enforcing a reverse Plaza Accord – when, in 1985, America de-facto broke the principles of the free market and `ordered` a devaluation of the US-dollar. Over the following eighteen months the Yen surged relentlessly from Y250/$ to Y130/$, choking-off Japan post-war export-led growth model. The scramble for domestic-demand reflation countermeasures led, at least in the eyes of my more conservative Japanese friends and politicians, to the `Bubble`. And yes, shortly after the Plaza Accord, Japan’s then Prime Minister launched an official `Asset Doubling` plan, centered on both macro stimulus and an unprecedented drive to deregulate financial markets. The rest, as they say, is history. But be that as it may…

More relevant to the Japan outlook today, Governor Kuroda is right on the economics.

Yes, there is a global supply shock. Both energy and food prices, as well intermediate- or component goods prices are forced higher by the war in Europe and the global economic security policy response it triggered. Japan is very much affected by this.

But no, here in Japan there is no evidence of demand-pull inflation. Japan is not America. Apologies for this obvious truism, but it cannot be emphasized enough if you want to understand why the BoJ is not afraid to go-it-alone and insists on a further de-coupling from the Fed. In my view, Governor Kuroda will change course only if or when Japan`s demand shows not just first signs of recovery, but enters a genuine self-sustaining up-cycle.

So what does the BoJ want to see?

Nominal GDP – which is a key summary indicator of what is actually going on in the real world of consumers, enterprises, financial markets and governments – stood almost 8% above the pre-pandemic trend in America in the latest available statistics, 1Q 2022. In Japan it was still stuck more than 3% below it. And as the first chart above shows, America has had a sharp V-shaped recovery from the pandemic trough, while Japan’s recovery has clearly stalled over the past year-and-a-half. Where America has been accelerating hard out of the pandemic, Japan has been merely coasting along.

Clear speak: the Fed had every reason to start hitting the brakes. It needs to reign-in a genuine above-trend demand cycle. Japan is obviously nowhere near this, so stepping on the monetary brakes is poised to be not just a mistake, but an admission that the basic policy conclusions offered by the `science` of economics no longer hold. Governor Kuroda is an avid student of both economic history and economic theory. He does not want to go down in history as yet another BoJ who tightens too early.

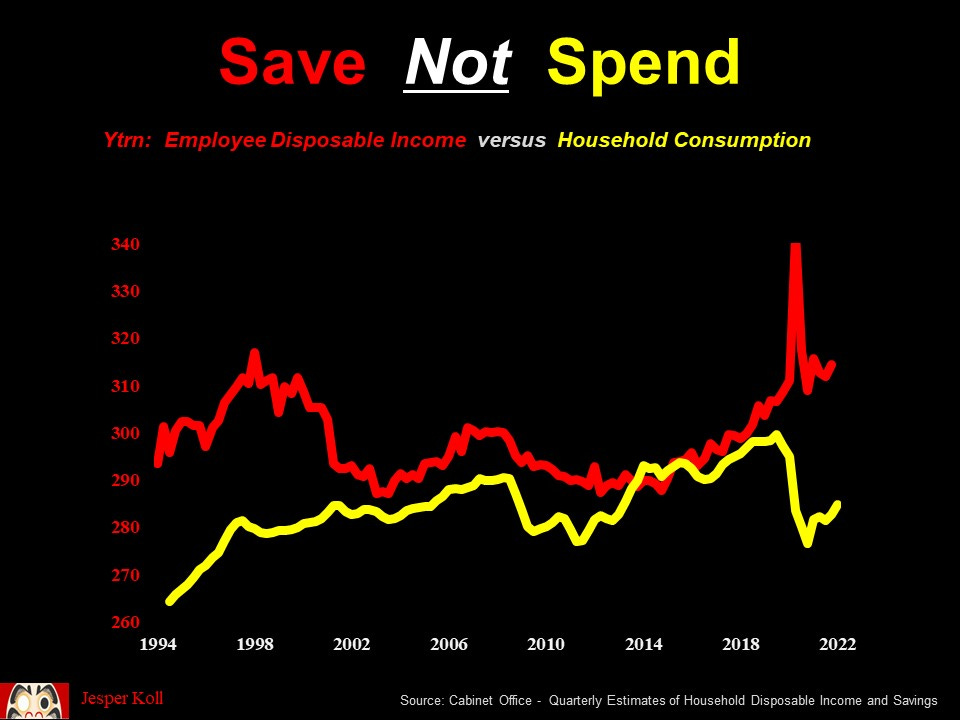

Save, not spend

The primary reason for still sup-par demand is weak consumption. It was still running approximately Y15 trillion, or about 2.75% of GDP below pre-pandemic trends in January-March 2022; and higher frequency updates do not point to a significant acceleration since. From are practical perspective, the BoJ`s `reaction function` from here will be primarily determined by whether and/or how fast this consumer `deflation gap` will close.

Disposable incomes are up

Importantly, Japanese consumption is not kept down by stagnating or falling incomes. While this is the standard narrative happily told by politicians and embraced by the media, the actual data very clearly points the other way: employee disposable incomes are solidly back up on the pre-pandemic up-trend.

Specifically, the pandemic countermeasures of direct transfers into citizens bank accounts did boost disposable incomes by the equivalent of almost 8% of GDP – this is the big spike up during 2020 in the following chart; but since then, we`re right back on the steadfast upwards trend in place since 2015/16. In contrast, consumption is still stuck at the bottom end of the 25-year range.

The Demographic Sweet Spot in action

This up-trend in employee incomes is powered by the much improved labor market in general, the rise in full-time rather than part-time employees in particular (as discussed in a previous Japan Optimist article, Demographic Sweet Spot).

No, wages are not rising, but incomes are because, unlike part-timers, full-timers do get paid the semi-annual bonus. Moreover, with the number of new jobs created up by about 1% every month, even per-capita disposable incomes are now on a modest uptrend of around 0.5-0.6%.

So yes, Japan’s private sector is creating jobs, offering better employment contracts and overall compensation; but no this positive dynamics is not translating into higher consumption. Japanese people still opt to save, not spend. In fact, the gap between incomes and consumption has not narrowed over the past four quarters (when the major distortions triggered by the pandemic were fading).

Lets stay pragmatic and practical, rather than speculate

Here I want to avoid falling into the trap of now trying to speculate and explain what may or may not determine Japan’s propensity to save –the arguments have not really changed over the 30+ years. Japan has often been accused of `under consumption` by trade negotiators, and there are more economics PhD thesis on Japan’s `mysterious` savings behavior and how to change it than there are Sushi bars in Shibuya. (I only wish more of these hardworking economists could afford to go to these bars; consumption would surely rise if stipends and grants allowed for a bit more in-the-real-world research, desho…).

So let’s take a practical approach. Let’s look at were exactly consumption has been weak? The answer is: not goods, but services. Consumption of goods is back up to pre-pandemic highs; but services consumption is still stuck far below it, by the exact same Y15 trillion that total consumption is still missing.

A Moment of Zen – all you need is Domestic Travel

The good news is that there is almost total clarity of where exactly those missing Y15 trillion come from: 国内旅行 - domestic travel. The various pandemic restrictions, government advisories and social conformity norms –there never was a true US-style lockdown in Japan because it is legally impossible for the government to restrict citizens freedom of movement—did force a collapse of domestic travel. Japanese spent Y21.9 trillion on domestic travel in pre-pandemic 2019. Last year, they spent slightly less than Y7 trillion. So from here, all we need to monitor is whether and/or how fast domestic travel recovers. The greater an uptrend towards the pre-pandemic Y22 trillion comes into view, the quicker Governor Kuroda’s `demand gap` argument disappears.

What about inbound travel?

Of course, inbound travel will also play a role, but it is of practically no importance for monetary policy. This is for two reasons:

First of all because inbound travel spending is much smaller than domestic travel spent, Y4.8 trillion versus Y21.9 trillion in peak-travel 2019. True, when Prime Minister Abe liberalized inbound travel in 2014/15, the net new marginal Yen spent by previously non-existent global tourists made a significant impact. Now, however, the marginal impact of domestic travel going from last year’s Y7 trillion back up to Y22 trillion will be the all-important force closing the domestic demand gap.

Second, because unlike domestic travel, international travel can be totally controlled by government rules and regulations. And indeed, here the government is following a prudent course of gradually, but steadily raising quotas for inbound tourists.

I say `prudent` here from an economic impact perspective – Japan has learned the lessons from the service disruptions and inflation surges triggered by the abrupt `from off to full-on` travel policies implemented in the US and elsewhere. But no matter how global entry rules are actually decided, in the here and now Japan’s managed phase-in approach to global travel allows suppliers to build capacity more-or-less in line with demand growth. The embarrassing at best, inflationary at worst shortages of airport baggage handlers, hotel staff or restaurant servers etc. observed in America or Europe are unlikely to be a problem in Japan.

Welcome to Japan, where nobody is afraid of managed competition; where there is a proud tradition of trust in Government and its ability to use of all the tools and opportunities available to avoid disruption and market uncertainty. No, I’m neither sarcastic nor optimistic in writing these lines, but very serious - Japan’s old and Japan’s new capitalism will always be marked by managed competition and a public sector mandate to drive resources towards common social capital. That’s why, in my view, Japan’s model of capitalism is capitalism that works.

Staying focused on what matters from here – the autumn domestic travel season

For the BoJ policy path from here, the key takeaway is that the strength of the recovery in domestic travel has become a most important indicator. It is the primary link still missing, but very much needed to close the gap between stagnation and sustainable demand recovery.

Specifically, domestic travel during the mid-August annual Obon family holiday season is poised to become an important trip-wire; another one will be the early autumn Momiji travel season in October. If, as I am hopeful, Japan’s retirees begin to travel again on these traditionally important occasions, Governor Kuroda is poised to be convinced that `the facts have changed`, and that therefore a policy change may become the right thing to do.

What about corporate investment?

Meanwhile, it is also important to keep an eye on the realities of corporate behavior in general, domestic business investment in particular. There is much hope for a return of `on shoring`, that the combination of a cheap Yen and national economic security priorities now commanding investments in new supply-chains and greater domestic self-sufficiency will lead to a new up-cycle in domestic capital investment.

Unfortunately, for now at least, these hopes are manifest only in the technocrats` wish-lists and vision papers. The hard data reveal a lackluster-at-best path of domestic corporate investment, with the absolute amount lingering at least 1% of GDP equivalent below the pre-pandemic uptrend; and, for now, showing no real sign of momentum or acceleration.

Will Governor Kuroda’s successor get a reason to revise-up Japan’s potential GDP?

For monetary policy, a sustained pick-up in capital spending is ultimately more important than a pick-up in the demand for consumer services. This because a capex boom raises the probability that the economy’s supply capacity is going to go up; and with it the potential growth rate of Japan.

At the same time, a new capex boom should make the BoJ even more relaxed as a rising potential growth rate should lead to a lower structural inflation path going forward. This, however, is poised to be a judgment call that –hopefully— Governor Kuroda’s successor will have to make. I say hopefully because right now there`s no evidence of a domestic capex boom; and it would definitely be in the post-Kuroda regime (his terms ends next spring) because no one serious would dare to upgrade Japan`s potential growth estimates until at least one year of a sustained capex uptrend is in evidence.

Clear speak: in the immediate future the strength of Japan`s consumer recovery is the all-important leading indicator for those trying to predict when (or weather) Governor Kuroda will become convinced Japan`s domestic demand has gained sufficient strength to achieve escape velocity, enough to propel him into the history books as the man who lead Japan out of its one-generation old deflation trap.

Thank you for taking the time to read - as always, comments & thoughts very welcome.

Many cheers ;-j

(1) Strictly speaking, this is not true: the collapse of Lehman Brothers forced a serious supply disruption in global financial markets, which quickly fueled a credit supply shock that almost brought down real economic agents, e.g. disruptions or trade finance etc. The global financial crisis was obviously very much a monetary phenomena. However, the current surge in food and energy prices has frightfully little to do with the Fed’s past or current monetary policy. It is obviously forced by Putin’s war, and the increasingly urgent and globally coordinated re-think of national economic security priorities it triggered. To argue the global chip shortage and consequently higher chip prices are nothing but an inevitable bit-part in the greater ‘always a monetary phenomena’ story does nothing but raise mistrust in, and cut the relevance of economic analysis for all us trying to make a living in the real-world.

Perhaps we should have another "GoTo" travel campaign before they relax inbound tourism quotas. This could spur the domestic travel market by incentivizing people to travel before popular tourist destinations are overrun.

❤️❤️❤️ Awesome read. Thank you, Jesper!